Teams aren’t paying anywhere close to that type of interest rate.

Financial institutions are fighting and bidding to get the business of an NFL franchise.

Financial institutions pay for sponsorship and may role some services in completely or at reduced rates.

Businesses borrow money to meet operational needs. To buy equipment, raw materials, inventory, etc.

For NFL teams the chief expense is personnel, the players. The players are the product and are what generates ALL of their income. So yes, funding the primary product does generate income.

The key for the wealthy is use as little of your own money as possible to drive additional income.

NONE of these teams owners are using their own money when you have a team worth billions to leverage. Every corporation has an interest expense that they manage.

None of these owners are hurting for their everyday living expenses.

The owners make choice on how they choose to manage the team, not because they can’t afford it.

The federal reserve base rate is 4.25%. A bank will add another 2.5% at least for their profit margin. My estimate is probably on the low side.

Businesses borrow money to fund growth. Any business that is borrowing to meet operational needs is in serious trouble, revenue should meet operational needs or a business is technically insolvent.

NFL revenues are largely fixed. Teams get the same TV money if they cheap out on their roster and finish 3-14 as if they spend excessively and go 14-3. Similarly, tickets are limited and fixed in how much money sales can generate. For a normal business, you buy a new property and open a new branch, hire new staff and that generates new, additional revenue. In the NFL, whatever you spend, you’re not generating a ton of new revenue. Yes, Lions fans would buy a ton of Garrett jerseys, but the $15 the Lions get from each jersey isn’t going to cover the cost of his contract, or the interest payments on borrowing the money to fund it.

It’s much cheaper and much more profitable to use your own money, rather than borrowing it, because then your business pays you interest rather than you paying a bank interest.

They do and they are. Absolutely. Mark Davis’ only asset of value is the Raiders. The money he takes out of the team is what he lives off. Any additional financial responsibilities the team takes on reduces what he has available to take out for himself. His net worth might be $5 billion, and he can borrow against that, but unless that borrowing is going to generate enough additional profit to cover the interest and then some, then it’s bad borrowing. Fronting players on big contracts generates a loss when you consider the time-value of money and net present values, because it won’t result in a sizable enough increase in revenue to justify it. He owns something that prints $15 million a year from him. For borrowing to be worthwhile he needs to know that the investment will lead to that number jumping to $25 million a year, the $15 million he was already getting, the $8 million to cover the interest, and an extra $2 million to make the whole thing worthwhile.

Those rates have nothing to do with individual business transactions.

Have you ever gotten a teaser 0% rate on a credit card?

What about the 0% interest rates on car loans?

Financial institutions can charge whatever they want to get business.

An NFL team is a premium client that leads to more business. Also, the loans are very low risk guaranteed by the value of the team and an organization with impeccable credit.

It’s done every day.

Virtually Every new car dealer in America has a loan on the vehicle on their lot.

Do you think every new car dealer has paid upfront for the hundreds of vehicles on their lot?

No it is not.

The wealthy can generate a higher rate of return investing their money and using someone else’s money at little or no interest.

Mark Davis is not going into his pockets to pay bonuses. And he is not hurting for his everyday living expense.

Come on Slay.

Mark Davis will not be taking cans back to the grocery store.

The Raiders are a multi-billion dollar entity that, like all NFL teams, operates with a guaranteed profit before they cut the lights on.

Interest expense is just part of doing business.

In some industries it is bigger and financial institutions fund everyday operations.

My point from the beginning is that teams make a choice whether to do void years, big bonuses, or other cap manipulation techniques.

It is either strategic, philosophy (accounting or principle) or frugality.

Every team is capable, it won’t hurt the everyday living expenses of ownership.

I never said a loss leader.

Large, very low risk loans can have a lower interest rate and still return substantial revenue.

Being the primary financial institution for an NFL team is worth the reduced revenue on an escrow loan.

The return that can be made on just holding and managing the payroll account, never the less all the other transactions and potentially all the players accounts is worth it.

Also possibly being the public banking face of the team with signage and co-branding.

Yes, a financial institution can take a little less on a very low risk escrow loan guaranteed by the value of a multi-billion dollar NFL team.

Nobody gives teaser rates on $200 million dollar loans. That would be something! PM me if you ever find a financial institution giving discounts on loans of more than six figures, let alone 8 or 9!

Yes, because selling each car generates new, additional income. It’s a whole different business model to an NFL team.

I work for a company that manages the wealth of the kind of people we’re talking about, one of our clients is the brother of the owner of an NFL team. That’s absolutely not how it works at all, they invest their own money by and large, that’s how it’s profitable. If they borrow at 8%, and invest with an 8% return then they’ve made $0. If they just invest at 8% with their own money then they make the 8%.

What do you mean, come on? Whether funding directly themselves, or borrowing to provide funding, the owner is taking on a significant liability. If you take a loan out for your kid’s college tuition, that’s not the bank funding it, it’s you funding it, because you’re going to be the one paying back the loan and taking on multiple years of financial obligations.

Average NFL team revenue is in the region of $650 million. If you want to pay out $200 million for three new contracts, then you’re not getting it out of that $650 million, because 90% or more of that has already been spent. To do that you need temporary funding and the only person who can provide that is the owner, and the cheapest way to do that is with their own money. But Mark Davis doesn’t have $200 million lying around, and borrowing it is expensive and there’s no return. Which is exactly why a lot of teams don’t mess with the cap like the Eagles have done, because the owner doesn’t have the appetite to either put their own money in or borrow money to do it.

Looking at the teams using option years most, I wonder how many of those option years were simple restructures of a player’s base salary and not large up-front bonuses to begin with.

Believe me, financial institutions buy business all the time with low rates on extremely large loans if the business case supports it.

Of course car sales are a different business, but you made the statement that if a business borrowed to meet operational needs it was insolvent. Just providing an example. The cars are the product just as the players are the product that drive NFL income.

I of course can’t speak for everyone. But most owners of multi-billion dollar business are not mixing personal funds with their business when it is a thriving profitable entity. when the enterprise is struggling the owner sometimes has to inject funds. This is definitely not the case with an NFL team.

The example of borrowing for a student loan has no relation to a business loan.

The business loan is only made when it can be shown that the net is profitable.

The business plan shows how the funds will be in vested and the rate of return.

The wealthy Individual borrows $100 backed by his good credit and many assets. It will cost him $5 for the year. His business plan shows how that $100 will be turned into $120 at the end of the year. The wealthy individual has made $15 with the banks money (and can write off a portion of the $5 as an interest expense). The wealthy individual didn’t tie up his own money. His own $100 is being invested and returns $112 at the end of the year.

The wealthy individual has made $27 (plus a tax savings with the interest expense).

If he had used his own money the wealthy person would have tied up his funds and only produced $20 net gain.

An NFL team is a profit machine. There is no need for an owner to inject personal funds.

I don’t want to go back and forth with you and dispute your brothers, uncles cousins friends comments.

Have a good night sir.

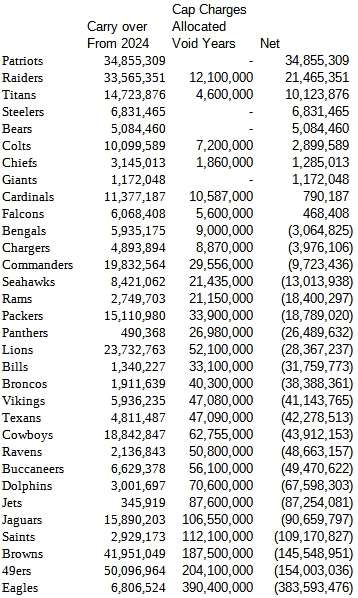

About a 3rd of the league has a positive adjustment. The Lions are middle of the pack at $28M . . . zero worries about extending Hutch/Kerby/others. Just need to make smart decisions (like the Eagles, but not the Browns or Saints).

Went through to compare the Lions to the Eagles. The Eagles are about $100M short of their total that Nick posted. I think it’s because of the complexity of their use of void years and OTC trying to record that data.

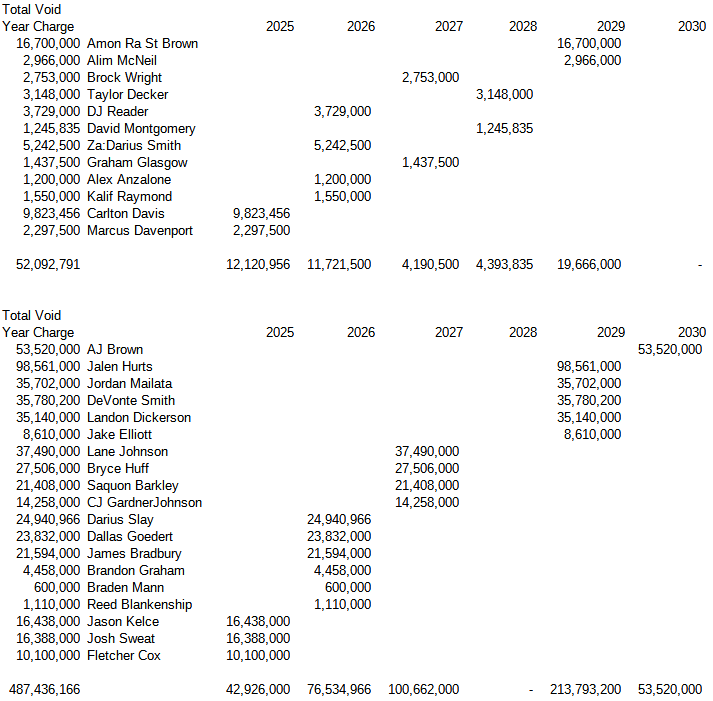

Looking at those contracts, half are tied to Saint and CD so for sure Saint will get a restructure at some point. Really only CD at $9M is a hit this year if not resigned. The rest are minimal at $25M. Appears to be some good cap management.

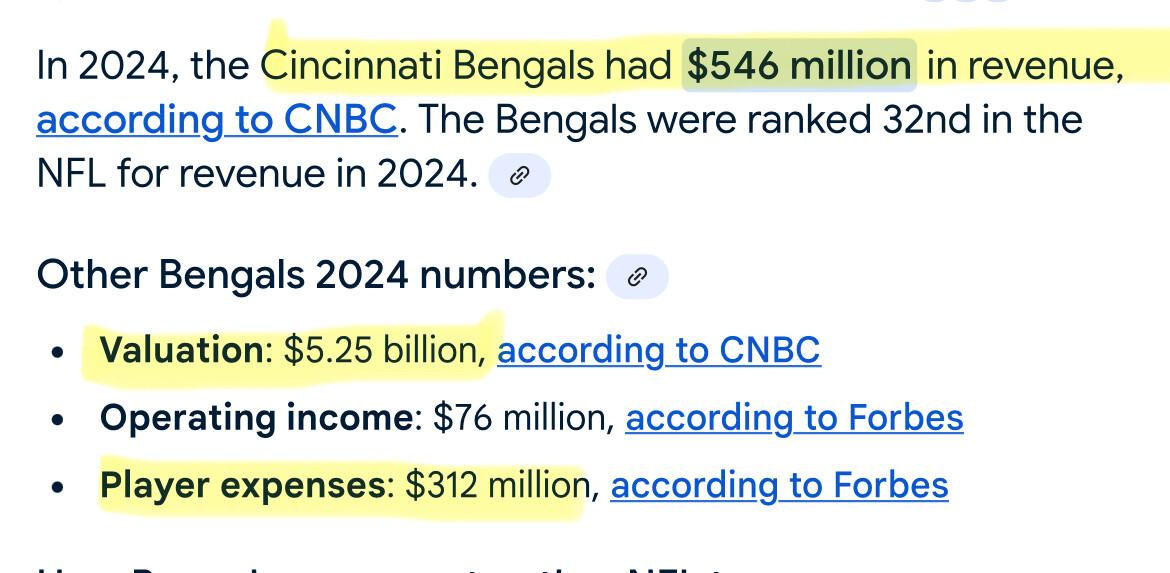

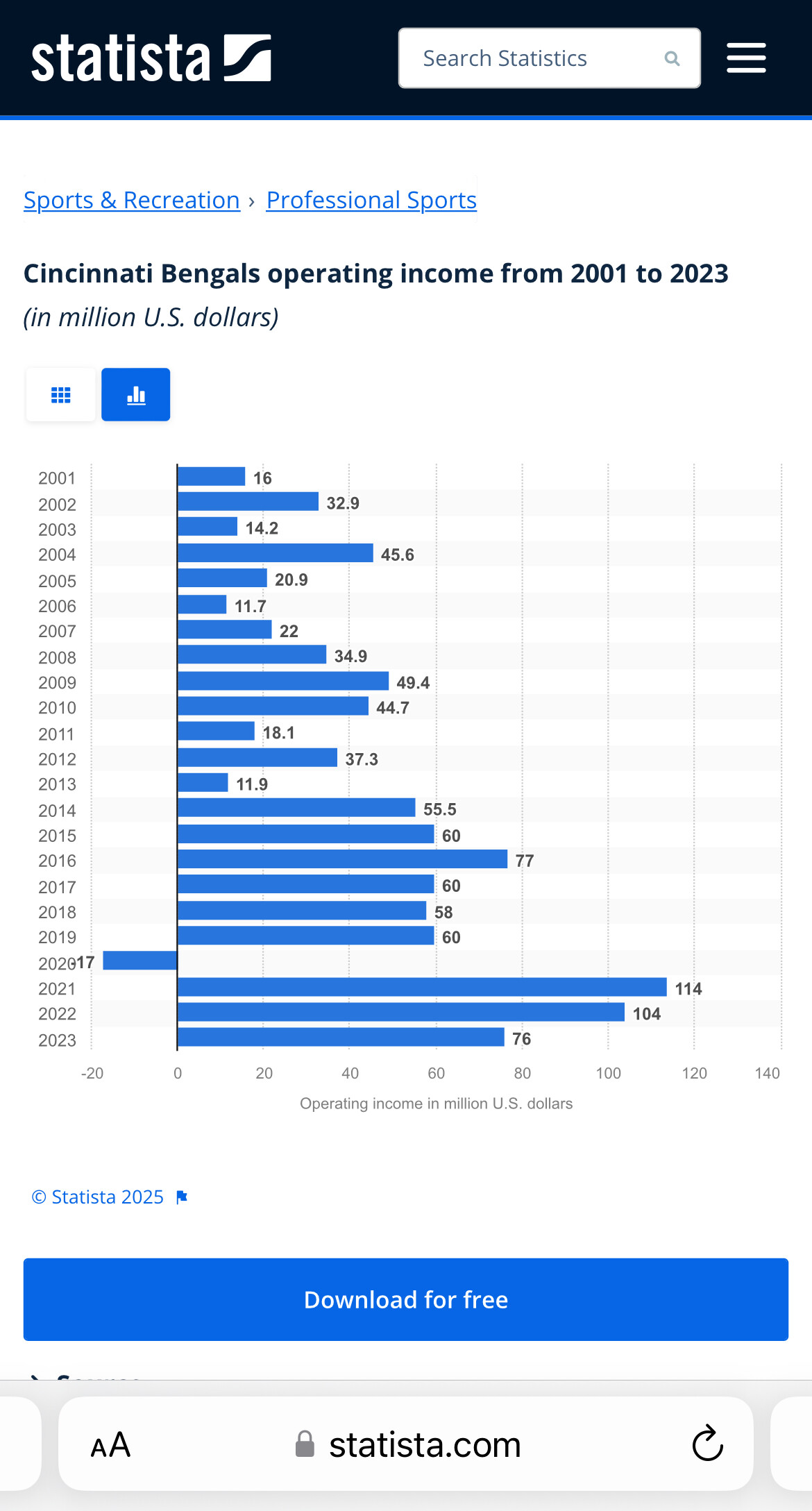

The Bengals have Hendrickson, Chase and Higgins up for contract renewals. Higgins has been tagged, and Hendrickson has been granted permission to seek a trade. The Bengals have the cap space to sign all three, both in 2025 and going forward, but they’re letting the NFL’s sack leader seek a trade.

Mike Brown / the Bengals don’t have the cash for all three contracts.

If Mike Brown didn’t have the cash flow…

he could sell ~10% of the team for ~ $500 million or more.

based on the franchise now valued at over $5 billion.